Canadian Real Estate Analysis 2020-2025

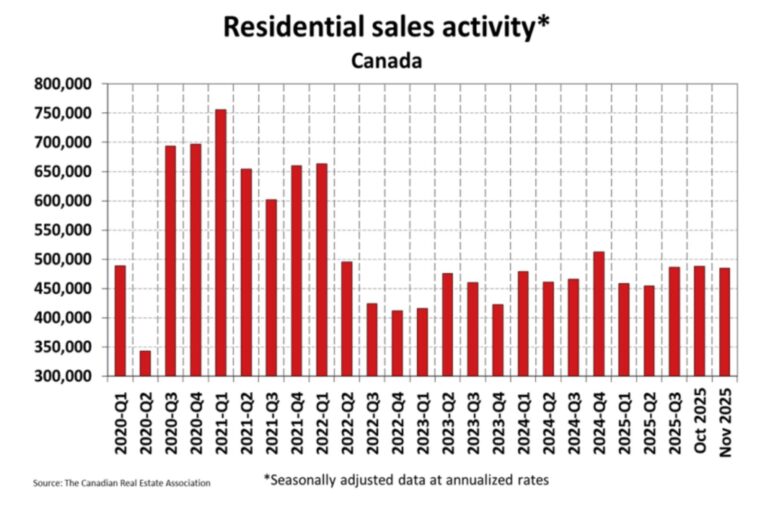

The national real estate landscape has undergone a profound transformation since the onset of the pandemic. As shown in the residential sales activity graph, the market moved from an unsustainable peak in early 2021 to a much more measured pace by the end of 2025.

1. The Pandemic Frenzy and Subsequent Correction (2020–2024)

The absolute summit of Canadian housing activity occurred in 2021-Q1, where seasonally adjusted annualized sales surpassed 750,000 units.

- The Surge: Record-low interest rates and pandemic-driven shifts in housing preferences created a “fear of missing out” (FOMO) that pushed 2021 home sales to record highs.

- The Retreat: To combat rising inflation, the Bank of Canada initiated one of its most aggressive interest rate hiking cycles in history starting in early 2022. This led to a significant market slump, with 2023 sales units dropping by 11.2% from 2022 levels.

2. Late 2025: A National Market in a “Holding Pattern”

As of November 2025, national residential sales activity has entered what economists call a “holding pattern”.

- Current Sales Activity: Home sales recorded on Canadian MLS® Systems were mostly unchanged since July 2025, showing only a slight 0.6% decline month-over-month in November.

- Inventory and Supply: There were approximately 173,000 properties listed for sale across Canada at the end of November 2025, an 8.5% increase from a year earlier.

- Market Balance: The national sales-to-new-listings ratio sits at 52.7%, which is well within the 45% to 65% range generally consistent with a balanced market.

- Price Softening: The National Composite MLS® Home Price Index (HPI) dipped 3.7% year-over-year in November 2025, suggesting that some sellers are increasingly making price concessions to finalize deals before year-end.

3. The Renewal Shock: A Critical Economic Pressure Point

- One of the most significant factors weighing on the 2025-2026 market is the massive wave of mortgage renewals.

- Volume of Renewals: Approximately 60% of all outstanding mortgages in Canada are expected to renew in 2025 or 2026.

- Payment Shock: Borrowers with a five-year fixed-rate mortgage renewing in 2025 or 2026 could face an average payment increase of 15% to 20% compared to their original December 2024 payments.

- Household Squeeze: For a typical $500,000 mortgage, this renewal shock can mean an increase of roughly $500 per month, or $6,000 per year, significantly tightening household budgets.

4. Regional Variation in a National Landscape

While the national trend is stable, there is a stark “tale of two markets” emerging across Canada.

- The “Unaffordable” Markets: Ontario and British Columbia continue to face significant challenges. Sales in these regions are expected to remain below their 10-year averages due to persistent affordability barriers.

- The Resilient Regions: Markets in Alberta, Quebec, and parts of Atlantic Canada have outperformed the national average. While Toronto prices fell roughly 7.2% annually by late 2025, Edmonton and Winnipeg saw gains of over 5%.

5. The 2026 Outlook: Rebound or Continued Lull?

Looking ahead to 2026, most major forecasts anticipate a gradual return of buyers to the market, though significant challenges remain.

- Projected Sales Rebound: CREA forecasts a 7.7% jump in national sales activity for 2026 as lower interest rates finally begin to release years of pent-up demand.

- Price Forecast: National home prices are expected to rise modestly by about 3.2% in 2026. However, some analysts like RBC expect national prices could decline slightly further by 0.7% in 2026 if inventory continues to build in BC and Ontario.

- Interest Rate Stability: The Bank of Canada held its overnight rate at 2.25% in December 2025, with many economists expecting it to hold steady through much of 2026.

Summary of the National State of Play

The Canadian real estate market in late 2025 is a far cry from the record-shattering volumes of 2021. While affordability has improved slightly due to recent rate cuts, the impending “mortgage renewal shock” and cautious economic prospects are likely to keep national sales activity at or below long-term averages well into 2026.

2020-2025 Real Estate Cycle FAQs

Contact us for a custom market evaluation based on the latest 2025 data.

Did Edmonton prices rise as much as Toronto or Vancouver from 2020-2025?

No, and that is a good thing for affordability. While Toronto and Vancouver saw massive spikes (and subsequent corrections), Edmonton experienced steady, moderate growth. This stability has kept our market accessible while other major cities became unaffordable for the average family.

How did the 2022 interest rate hikes affect Edmonton compared to the rest of Canada?

Because Edmonton home prices are significantly lower (averaging ~$400k-$500k vs. $1M+ in Toronto), the impact of rate hikes was less severe here. Edmonton buyers could still qualify for mortgages that would be impossible in higher-priced markets, keeping our sales volume relatively stable.

Is 2025 a good year to buy a home in Edmonton?

Yes. The analysis shows that while the national market is cooling, Alberta is seeing record migration. This suggests that demand in Edmonton will remain strong, potentially driving prices up as inventory tightens, making now a strategic time to buy before the “Alberta Advantage” closes the price gap.

What is the forecast for Canadian real estate in late 2025 and 2026?

Most analysts predict a return to “balanced” conditions nationally, with modest price growth. However, Edmonton is expected to outperform the national average due to its affordability and the influx of buyers moving from Ontario and BC.

Did the ban on foreign buyers affect the Edmonton market?

Its impact was minimal in Edmonton compared to Vancouver or Toronto. Our market is driven primarily by local buyers and interprovincial migrants (Canadians moving from other provinces), rather than international speculation.